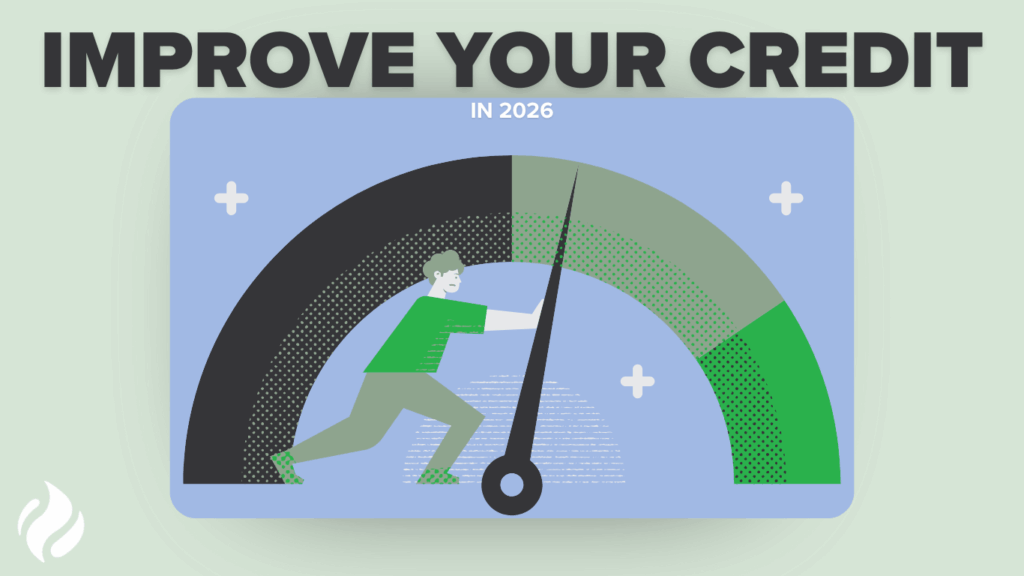

If you’re thinking about installing solar panels, your credit score can have an impact on your options. Solar is the next step to lower your energy costs over time. However, qualifying for the best loan terms often depends on your credit history. Learning how to improve your credit before applying for solar financing can increase your chances of approval. It may even help you secure better interest rates and payment options.

How Your Credit Score Affects Solar Financing

Your credit score is based on several factors that lenders use to evaluate your financial habits. Payment history accounts for 35% of your score, making it the most important factor. Paying your bills on time is essential because late or missed payments can lower your score significantly.

Credit utilization makes up 30% of your score. Keeping your credit card balances below 30% of your available credit shows lenders that you manage debt responsibly. The length of your credit history contributes 15%. That means maintaining older accounts can strengthen your overall profile.

New credit represents 10%, which is why opening multiple accounts in a short period can negatively affect your score. The remaining 10% comes from your credit mix. This means the combination of credit cards, auto loans, and mortgages. All of these can help prove responsible borrowing.

How to Improve Your Credit for Better Solar Loan Options

One of the most effective ways to improve your credit is by paying down high-interest or high-balance accounts first. If you lower your overall credit utilization, it can help your score increase over time. Making small extra payments each month can make a noticeable difference.

Setting up automatic payments is another simple step that helps protect your credit. Missing a payment, even accidentally, can reduce your score by dozens of points. It is best to enroll yourself in an auto-pay system. Even paying the minimum amount helps ensure your account’s credibility.

It’s also important to review your credit report regularly. You can request a free copy of the Annual Credit Report. Even more, you can try the Federal Trade Commission (FTC) and check for free credit reports. Check for errors, outdated information, or fraudulent activity to keep yourself safe. Correcting inaccurate information may improve your credit score more quickly than expected.

While it may seem like a good idea to close credit cards you no longer use, keeping older accounts open can actually benefit your credit. However, closing long-standing accounts may reduce your available credit. It could also shorten your credit history, which can affect your score.

Why Better Credit Can Help You Save with Solar

There are plenty of ways for homeowners to pay for solar. You can try cash purchases, solar loans, and even Power Purchase Agreements (PPAs). A loan is the fastest way to begin enjoying the benefits of renewable energy. You can even try out our solar leasing agreements for a more structured payment system.

Stronger credit scores can help you qualify for plenty of benefits. This can include lower interest rates, flexible payment options, and faster loan approvals. Even better financing terms can also make it easier to start saving on energy bills.

Improving your credit is an investment. Not only in your financial future, but also for your home’s energy efficiency. When you’re ready, our team can help you review financing options that fit your goals. We’re here every step of the way to support your transition to renewable energy. Contact us now and learn what solar could do for your home.

Sources

- Experian — Ways to Improve Your Credit (2025). experian.com

- Experian — How to Improve Your Credit Score (2025). experian.com

- Experian — How Rent and Utility Payments Can Help You Build Credit (2025). experian.com

- NerdWallet — Raise Your Credit Score Fast (2025). nerdwallet.com

- U.S. Bank — 6 Tips on How to Improve Your Credit (2025). usbank.com

- LendingClub — How to Improve Your Credit Score (2025). lendingclub.com

- Investopedia — 5 Secrets to Eliminate Credit Card Debt Quickly (2025). investopedia.com

- PFCU – Philadelphia Federal Credit Union — The Ultimate Guide to Fixing Bad Credit (2025). pfcu.com

- MyCVCU – My Community Credit Union — Understanding Credit Scores: Tips for Improving and Maintaining a Healthy Credit Score (2025). mycvcu.org

- MIWF — Improve Your Credit Score (2025). miwf.org